Traditional IRA Contributions - Guide to

Modeling IRA Savings Over Time

Most everyone knows you

can contribute to either a Traditional IRA or a Roth IRA, but how will that affect

YOUR SPECIFIC retirement? On this page we will show you how our software can be

used to model the ongoing savings you make to a Traditional IRA or a Roth IRA,

as well as how that will affect your retirement income picture. Let's get started.

TRADITIONAL IRA

CONTRIBUTION LIMITS |

|

Tax

Year

|

Regular

Contribution Limit

|

Additional

Catch-up Contribution for those 50 & Over

|

| 2005 |

$4,000

|

$500

|

| 2006 |

$4,000

|

$1000

|

| 2007 |

$4,000

|

$1000

|

| 2008 |

$5,000

|

$1000

|

| 2009-2012 |

$5,000

|

$1000

|

| 2013 |

$5,500

|

$1000

|

|

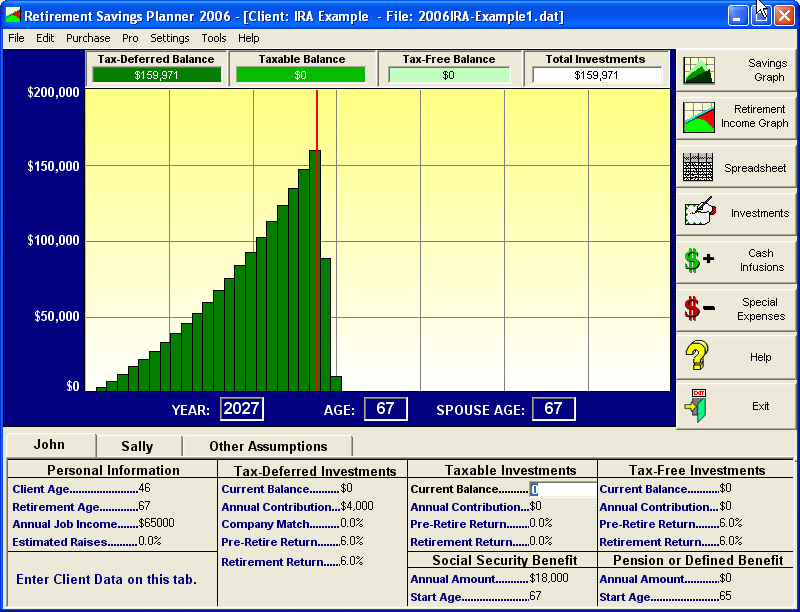

Step 1: In our software

we create a new plan for a "John and Sally Sample". John is 46 and makes

$65,000 and will contribute the maximum to a Traditional IRA until he retires

at age 67. Sally we assume is also 46 and makes $25,000 and will also retire at

67. The maximum John can contribute for the 2005 tax year is $4000. We enter an

Annual Contribution to his IRA of $4,000. And we can see that at retirement age

65 he will have accumulated $159,971 assuming he achieved an average annual return

of 6%.

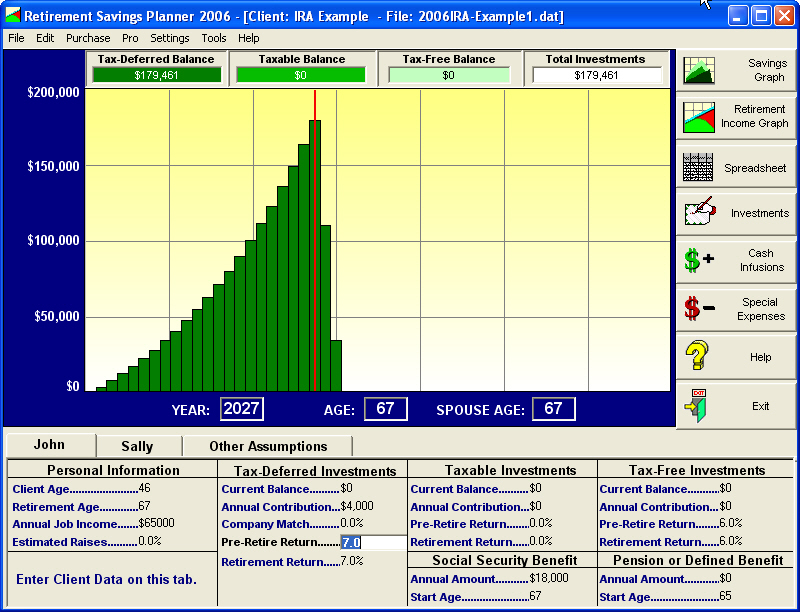

Step 2: If he could

get a 7% return, then he would have accumulated $179,461.

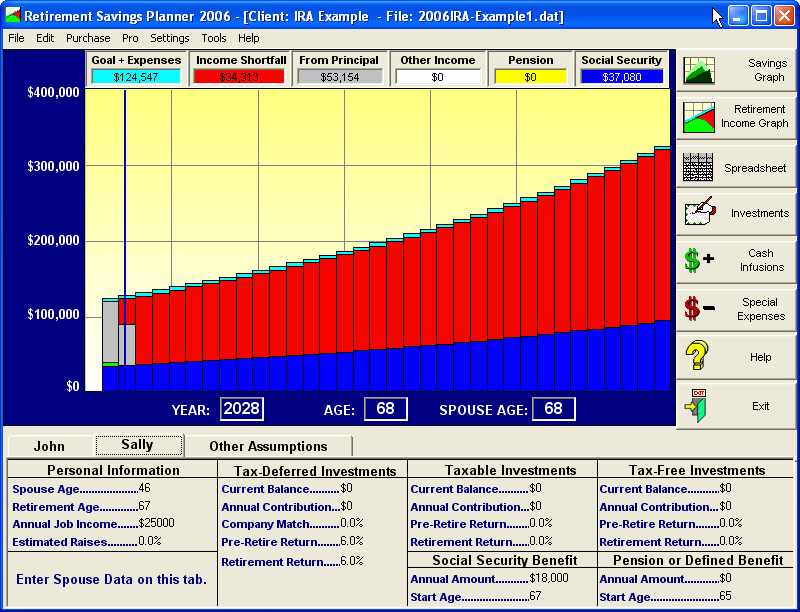

Step 3: We then flip

to the Retirement Income Graph to see how this savings plays out in retirement.

If we assume a $65,000 retirement income need at a 3% inflation rate, the accumulated

savings only lasts less than 2 years, assuming he also gets a basic Social Security

benefit.

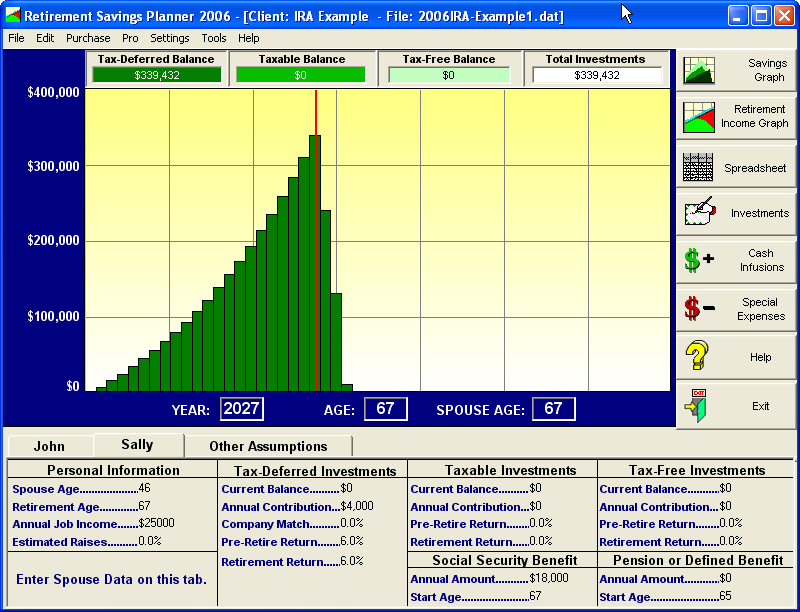

Step 4: Let's add

a $4,000 annual contribution for his wife Sally and also set her investment return

to 6% annually on average. As you can see below they now accumulate $339,432 for

their retirement.

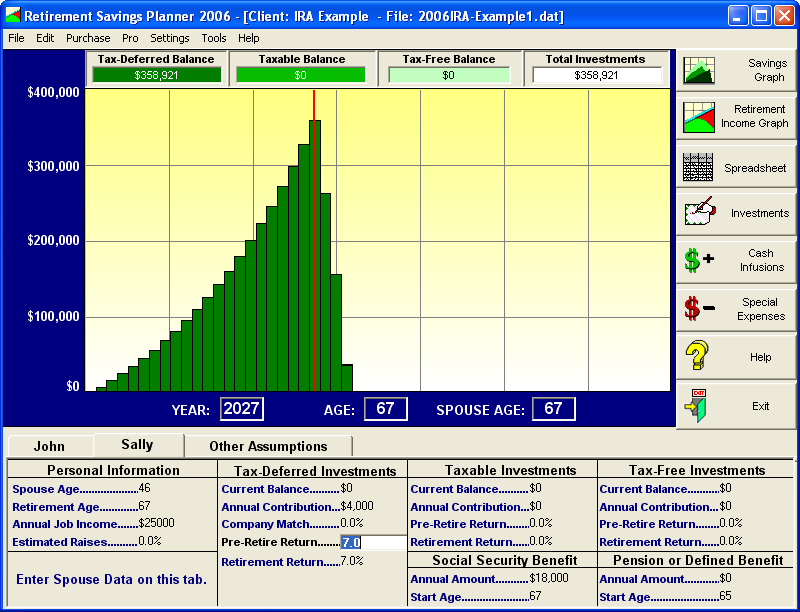

Step 5: What if we

assume a 7% investment return for Sally's IRA too. Then as you can see below they

will accumulate $358,921.

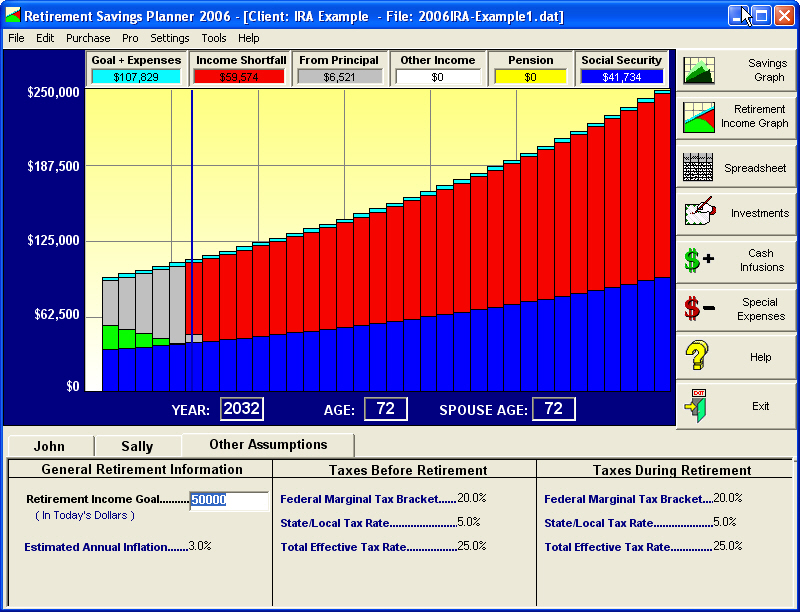

Step 6: We flip back

over to the Retirement Income Graph and scroll our mouse to the first red bar

we see. That is the first year where they start having "shortfalls"

in retirement. As you can see the plan now gets them part way into their 4th year

of retirement before they run out of savings.

Step 7: What if they

tighten their expense belts and live on less than $65,000 annually during retirement.

Since their current income is $90,000 they are already dramatically living on

less. If we cut that back to just $50,000, then their income lasts until age 72

instead of age 70.

Step 8 - ROTH IRA EXAMPLE:

What if we did the same scenario but instead contributed to a Roth IRA, instead

of a Traditional IRA? We will make a simplifying assumption that we are not evaluating

the tax deduction, if any, for the Traditional IRA. We are just going to consider

the same amount going into a Roth IRA. When you reach age 70.5 you won't have

to take out any Required Minimum Distributions, but more importantly the distributions

are tax free as long as you are over age 59 ½. Thus, your money should

last longer. In this case they will accumulate the same $358,921 but those dollars

will be sitting in the Tax-Free investments pool. When we withdraw them in retirement,

no taxes will be due! In which case their money lasts until the beginning of age

74.

This excercise shows

you:

1). why people are not enamored with IRAs because the contribution limits prevent

you from accumulating a substantial retirement nest egg.

2). how easy it is to model very specific IRA illustrations for someone's real

situation.

Unlike "other programs",

ours is Quick, Simple and Visual and let's you instantly see changes in real-time.

It's so simple that anyone can use it. We guarantee that or your money back.

Please

download our demo or view our tutorial video.

Retirement Savings Planner Software

Download

FREE Trial

Your License Subscription includes:

- all updates and enhancements

for one year

- free technical support

via email or phone

Personal

vs. Couples vs. Professional Edition

|

Personal

Edition

|

Couples

Edition

|

Professional

Edition

|

| New User Price - See ORDER FORM for latest prices |

-

|

-

|

-

|

| 90-Day Money Back Guarantee |

|

|

|

| Quick, Simple, Visual retirement

planning |

|

|

|

| Print Detailed Reports |

|

|

|

| Export Data to Excel |

|

|

|

| Email and Phone Support |

|

|

|

| Enter unlimited number

of investments |

|

|

|

| Number of retirement plans

you can create |

1

|

1 with

spouse

|

unlimited

|

| Enter Personal Data for

Spouse Separately |

|

|

|

| Specify Owner of Investments

as You/Spouse |

|

|

|

| Continue Contributions

and Returns after One Spouse retires and the other keeps working |

|

|

|

| Enter Separate Social Security

and Pension values for each Spouse |

|

|

|

| View Spouse Combined Retirement

Income analysis |

|

|

|

| Print Spouse information

on Detailed Report |

|

|

|

| Customize printed reports

with name, company, and contact info |

|

|

|

| Customize disclaimers on

printed report |

|

|

|

| Life Insurance Needs

Calculation |

|

|

|

| Added Savings Solver

(additional savings required to eliminate shortfalls) |

|

|

|

Required Minimum Distribution

Calculations |

|

|

|

| Add digital photo of

clients to Client info |

|

|

|

Many more exciting enhancements

will be coming this year! Anyone who buys will get updates for ONE FULL YEAR from

date of purchase.

|